Finance

Home Loan Refinancing : Eligibility, Interest rate and Apply Process

Home Loan Refinancing: Homeownership is one of the biggest financial commitments most people make in their lives. Over time, circumstances change — interest rates fluctuate, incomes grow, or financial goals shift. This is where refinancing a home loan comes into play. Refinancing allows homeowners to replace their existing mortgage with a new one, often with better terms.

In this article, we will explore what home loan refinancing is, its benefits and drawbacks, when it’s the right time to refinance, and how you can go about it successfully.

What is Home Loan Refinancing?

Home loan refinancing is the process of taking out a new mortgage to pay off your existing home loan. Typically, the new loan has better terms — lower interest rates, longer tenure, or smaller EMIs.

Refinancing a home loan allows homeowners to replace their existing mortgage with a new one, usually at better terms. This can help reduce interest rates, lower monthly EMIs, and even shorten the loan tenure. Many people refinance to take advantage of falling interest rates, improve cash flow, or switch from floating to fixed rates for stability. In India, several banks and financial institutions offer attractive refinancing or balance transfer options, often with minimal processing fees. However, it’s essential to carefully evaluate the total savings after factoring in any charges or penalties. Done wisely, refinancing can offer significant long-term financial benefits.

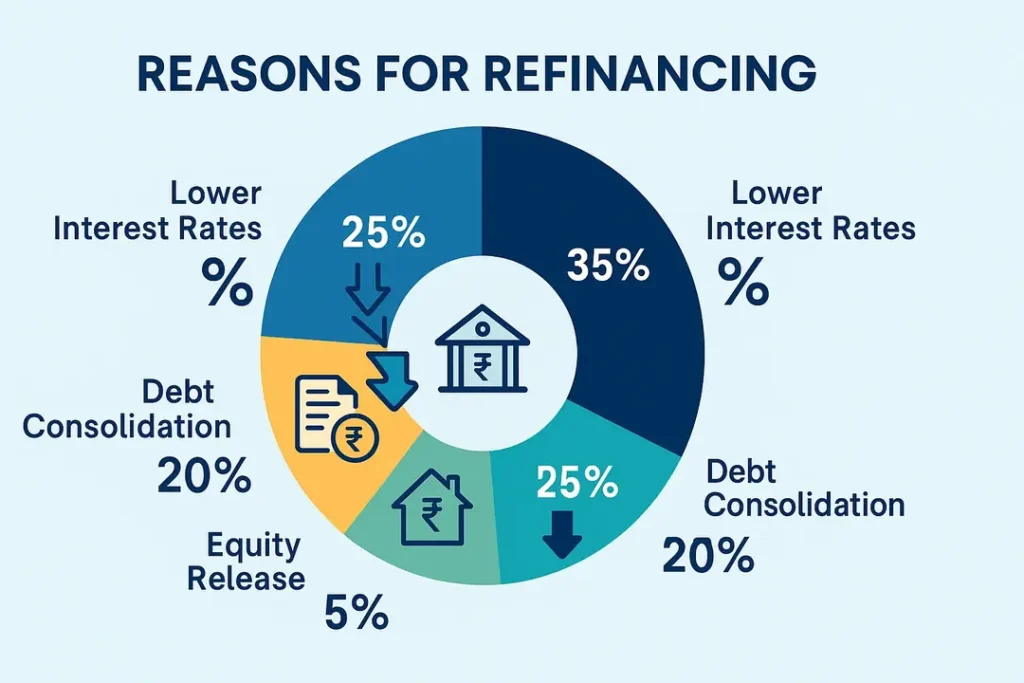

Why Do People Refinance Home Loans?

There are multiple reasons why homeowners choose to refinance:

- Lower Interest Rates: Interest rates may have dropped since you first took your loan. Refinancing at a lower rate can save you lakhs over the loan tenure.

- Reduced EMIs: Lower interest rates or extended loan tenure can significantly reduce monthly EMI payments, freeing up cash for other expenses or investments.

- Change Loan Type: You may want to switch from a floating rate to a fixed rate loan (or vice versa) depending on market trends.

- Debt Consolidation: Some homeowners consolidate other debts (credit card, personal loan, etc.) into their home loan at a lower interest rate, simplifying repayments.

- Home Equity Release: You may refinance to unlock the equity you’ve built up in your home to fund major expenses like education, weddings, or business ventures.

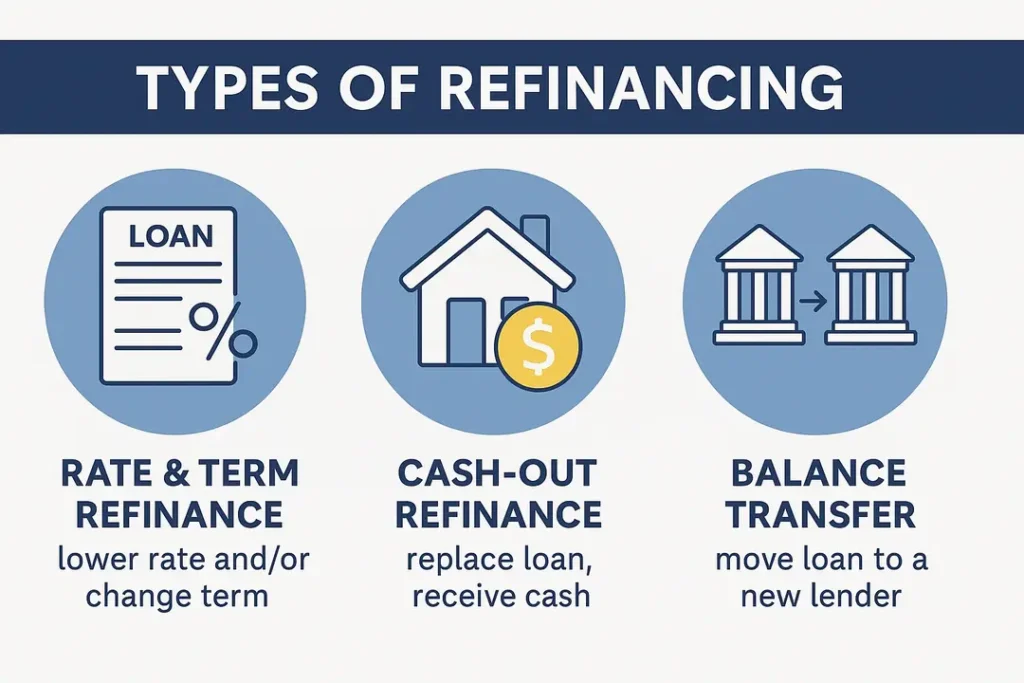

Types of Home Loan Refinancing

- 1. Rate and Term Refinance: Most common; replaces your old loan with a new one offering better interest rates or different loan tenure.

- 2. Cash-Out Refinance: Allows you to borrow more than you owe and receive the difference in cash, using your home’s equity.

- 3. Balance Transfer: You shift your loan from one lender to another offering better terms. Many banks in India actively offer balance transfer schemes.

Benefits of Home Loan Refinancing

✅ Significant savings over the loan tenure

✅ Lower EMIs and better cash flow

✅ Shorter loan term — debt-free sooner

✅ Access to home equity

✅ Better control over loan structure

Disadvantages of Refinancing

❌ Processing fees and prepayment penalties

❌ Risk of higher debt if not managed wisely

❌ Possible higher interest rates in the future (for floating rate loans)

❌ Lengthy documentation process

When Should You Consider Refinancing?

- Interest rates have dropped by at least 0.5% to 1%

- Your credit score has improved significantly

- You plan to stay in your home for several years

- Your financial goals or cash flow needs have changed

- You want to switch from floating to fixed rate or vice versa

Step-by-Step Guide to Refinancing

Step 1: Evaluate Your Current Loan

Check your existing loan details: remaining tenure, outstanding principal, interest rate, and EMIs with Home loan Refinancing Calculator.

Step 2: Research Market Offers

Compare different banks and NBFCs. Use online tools to calculate potential savings.

Step 3: Calculate Cost vs. Savings

Factor in processing fees, legal charges, insurance premiums, and potential penalties.

Step 4: Apply for the New Loan

Submit the required documents:

- KYC (Aadhaar, PAN)

- Income proof

- Property papers

- Existing loan statements

Step 5: Complete Legal and Technical Verification

The lender will verify the property value and your creditworthiness.

Step 6: Loan Disbursal and Closure

The new lender will pay off your old loan, and your EMI payments will begin with the new lender.

Current Scenario of Home Loan Refinancing in India (2025)

With RBI maintaining a steady repo rate and increased competition among lenders, refinancing has become highly attractive. Many banks like SBI, HDFC, ICICI, Axis, and NBFCs are offering balance transfer options at rates as low as 8% to 9% p.a., making it a lucrative option for many borrowers.

| Bank | Interest Rate (2025, p.a.) |

|---|---|

| SBI | 8.30% |

| HDFC Bank | 8.40% |

| ICICI Bank | 8.35% |

| Axis Bank | 8.45% |

| Kotak Mahindra | 8.50% |

| PNB | 8.60% |

Conclusion- Home loan Refinance

Refinancing a home loan can be a smart financial move if done carefully. It offers opportunities to save money, reduce EMIs, or free up cash for other priorities. However, it requires thorough research, careful calculations, and awareness of potential pitfalls. With careful planning, refinancing can help you achieve greater financial stability and peace of mind.

Application Form

Loan App1 year ago

Loan App1 year ago10 Best instant Loan Apps in India 2025: बस 10 मिनट में मिलेगा लोन

- Personal loan1 year ago

Piramal Finance Loan Apply Now: 10 लाख रूपये का इंस्टेंट पर्सनल लोन

- Govt Loan9 months ago

Business Loan: सरकार से लोन कैसे प्राप्त करें, मिलेगा ₹50 लाख तक बिजनेस लोन | PMEGP Loan Process

- Personal loan1 year ago

Emergency Loan Kaise Milega: अब मिनटों में आयेगा लोन का पैसा आपके अकाउंट में!

- Personal loan1 year ago

Aadhar Card Se Loan Kaise Le: आधार कार्ड से मिनटों में मिलेगा 50 हजार से अधिक का लोन, जानें आवेदन प्रक्रिया

- Loan App1 year ago

Kreditbee Loan App Review: क्रेडिटबी से ₹5 लाख का पर्सनल लोन कैसे लें

- Finance1 year ago

SBI Personal Loan कैसे लें, जानिए इसकी योग्यता शर्ते, ब्याज़ दरें, और आवेदन प्रक्रिया

- Loan App1 year ago

RapidRupee ऐप से पर्सनल लोन कैसे लें? क्या रैपिडरुपी ऐप सुरक्षित है?